Le sildénafil présent dans Kamagra exerce une inhibition réversible de la PDE5, modulant la cascade GMPc et favorisant une vasodilatation localisée. L’absorption digestive varie selon la forme utilisée, comprimés classiques ou gels oraux. La distribution tissulaire est large et la liaison protéique élevée, avoisinant 96 %. La métabolisation hépatique génère un métabolite actif contribuant à l’effet pharmacologique global. La demi-vie reste courte, avec disparition plasmatique en quelques heures. Les interactions significatives concernent surtout les nitrés organiques et inhibiteurs puissants du CYP3A4. Dans les publications techniques, kamagra en ligne est souvent cité dans le cadre d’analyses comparatives portant sur les différences de formulations et de cinétique d’absorption.

Microsoft word - sun-prandin litigation verdict-final

Sun Pharmaceuticals ACCUMULATE Prandin patent case: A positive win Event: The US Supreme Court ruled in favor of Caraco, US subsidiary of Sun

Pharma, in its patent litigation against Novo Nordisk’s diabetes drug Prandin.

The court concluded that Caraco can seek correction of Novo’s inaccurate

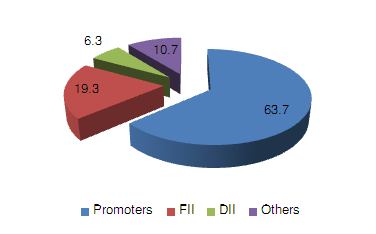

Stock Info

use-codes over the drug; however, the court’s ruling on whether the correction

applies to Caraco’s labeling is still pending.

Background: Prandin is approved by the USFDA for three specific uses, but

Novo’s original patent covered only one usage. Thus, post filing the ANDA for

gPrandin, Caraco also filed a section 8 statement which seeks approval for two

other uses not covered by the patent listed in the Orange Book. Novo then

changed its use-code for the ‘358 patent’, broadening the scope of the use-

code to cover all the three approved uses. Usually, the USFDA approves the generic drug within the scope of the use-codes and does not determine the

scope of the same. Post favorable ruling, Caraco could get approval for the

two other uses without infringing Novo’s patent.

About Prandin: Prandin (known as Repaglinide is used to cure diabetes) has a Stock Performance

market size of US$230mn in US and its patent is held by Novo Nordisk till

SUN PHARMA

2018. Caraco holds an FTF status on the drug and is still awaiting the final

approval from the USFDA (post the site transfer).

Impact: We believe that Sun Pharma can clock US$30mn in terms of revenues

from the gPrandin supply during exclusivity. While, Novo has filed its appeal Shareholding Pattern (%)

against Caraco in 1QCY2012, the final approval could take some time, leaving options open for an “at-risk launch” for Sun Pharma.

Outlook and Valuation

We view this ruling as a benchmark for the generic companies where they can appeal for either invalidity of the patent and/or counterclaim brand’s inaccurate use

codes. This procedure could stall the unnecessary delays caused to stop generic companies in marketing their drugs.

We believe that the positive ruling could pave way of faster approval for gPrandin.

Along-with strong product pipeline (Uroxatral, Duloxetine, Pregablin, Eszopiclone,

Stock Price Chart

Memantine) spread across FY2013E and FY2014E, such incremental opportunities

would boost the gains of the company. We remain positive on Sun Pharma, given

its steady performance, superior brand franchise in the domestic market, growth

prospects in the US market and the excellent M&A track record.

We factor high tax liability post the budget in our FY2013E numbers and introduce FY2014E numbers in this note and roll over our target price on new projected EPS. We recommend Accumulate on the stock with the price target of Rs650. Sun is

currently trading at 25x and 20.4x its FY2013E and FY2014E EPS respectively.

Risks to the view

Delay in product approvals and higher than expected liability on Protonix

Analyst: Sapna Jhavar sapna.jhavar@relianceada.com

Lower than expected performance from Taro

Net Revenues Net income (reported) Valuations (X) EV/EBITDA Profit & Loss Statement Balance Sheet Y/E March (Rs cr) Y/E March (Rs cr) Gross sales SOURCES OF FUNDS Total Expenditure Shareholders’ Funds Total Liabilities APPLICATION OF FUNDS Net Block Investments Recurring PBT PBT (reported) Net Current Assets PAT after MI (reported) Total Assets Basic EPS (Rs) Cash Flow Statement Key Ratios Y/E March (Rs cr) Y/E March Valuation Ratio (x) Cash Flow from Operations Cash Flow from Investing Per Share Data (Rs) Cash Flow from Financing Opening Cash balances Returns (%) Closing Cash balances Turnover ratios (x) General Disclaimers: This Research Report (hereinafter called ‘Report’) is prepared and distributed by Reliance Securities Limited (RSL) for information purposes only. The views herein constitute only the opinions and do not constitute any guidelines or recommendation and should not be deemed or construed to be neither advice for the purposes of purchase or sale of any security, derivatives or any other security through RSL nor any solicitation or offering of any investment /trading opportunity on behalf of the issuer(s) of the respective security(ies) referred to herein. These information / opinions / views are not meant to serve as a professional investment guide for the readers. No action is solicited based upon the information provided herein. Recipients of this Report should rely on information/data arising out of their own investigations. Readers are advised to seek independent professional advice and arrive at an informed trading/investment decision before executing any trades or making any investments. This Report has been prepared on the basis of publicly available information, internally developed data and other sources believed by RSL to be reliable. RSL or its directors, employees, affiliates or representatives do not assume any responsibility for, or warrant the accuracy, completeness, adequacy and reliability of such information / opinions / views. While due care has been taken to ensure that the disclosures and opinions given are fair and reasonable, none of the directors, employees, affiliates or representatives of RSL shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary damages, including lost profits arising in any way whatsoever from the information / opinions / views contained in this Report. Risks: Trading and investment in securities are subject market risks. There are no assurances or guarantees that the objectives of any of trading / investment in securities will be achieved.

The trades/ investments referred to herein may not be suitable to all categories of traders/investors. The names of securities mentioned herein do not in any manner indicate their prospects

or returns. The value securities referred to herein may be adversely affected by the performance or otherwise of the respective issuer companies, changes in the market conditions, micro

and macro factors and forces affecting capital markets like interest rate risk, credit risk, liquidity risk and reinvestment risk. Derivative products may also be affected by various risks including

but not limited to counter party risk, market risk, valuation risk, liquidity risk and other risks. Besides the price of the underlying asset, volatility, tenor and interest rates may affect the pricing

Disclaimers in respect of jurisdiction: The possession, circulation and/or distribution of this Report may be restricted or regulated in certain jurisdictions by appropriate laws. No action has

been or will be taken by RSL in any jurisdiction (other than India), where any action for such purpose(s) is required. Accordingly, this Report shall not be possessed, circulated and/or

distributed in any such country or jurisdiction unless such action is in compliance with all applicable laws and regulations of such country or jurisdiction. RSL requires such recipient to inform

himself about and to observe any restrictions at his own expense, without any liability to RSL. Any dispute arising out of this Report shall be subject to the exclusive jurisdiction of the Courts

Disclosure of Interest: The research analysts who have prepared this Report hereby certify that the views /opinions expressed in this Report are their personal independent views/opinions in

respect of the securities and their respective issuers. Neither RSL nor the research analysts did have any known direct /indirect conflict of interest including any long/short position(s) in any

specific security on which views/opinions have been made, during the preparation of this Report.

Copyright: The copyright in this Report belongs exclusively to RSL. This Report shall only be read by those persons to whom it has been delivered. No reprinting, reproduction, copying,

distribution of this Report in any manner whatsoever, in whole or in part, is permitted without the prior express written consent of RSL.

Important These disclaimers, risks and other disclosures must be read in conjunction with the information / opinions / views of which they form part of. Reliance Securities Limited is a Stock Broker with Bombay Stock Exchange Limited (SEBI Registration Nos. INB011234839, INF011234839 and INE011234839); with National Stock Exchange of India Limited (SEBI Registration Nos. INB231234833, INF231234833, and INF231234833); and with MCX Stock Exchange Limited (SEBI Registration No. INE261234833)

Parallel Trade of Pharmaceutical Products and EU “The price of pharmaceutical products in some Member States is typically much higher than in others. It is the price differentials between Member States which create the opportunities for parallel trade” (Advocate General Jacobs’ Opinion in C-53/03, Syfait I, ¶ For the European Commission “the scope of EC competition law is

Verslag Codex Committee on Veterinary Drugs in Foods Minneapolis, 26-30 aug 2013 Algemeen Tijdens de 21e bijeenkomst van de CCRVDF waren 61 landen vertegenwoordigd, waarvan 13 landen van de EU. Er is flinke vooruitgang geboekt op de ontwikkeling van wereldwijde standaarden voor diergeneesmiddelen waarbij risico’s voor de volksgezondheid bestaan als deze in voedsel terecht komen. Voor

Sun Pharmaceuticals

Sun Pharmaceuticals  Profit & Loss Statement

Profit & Loss Statement  General Disclaimers: This Research Report (hereinafter called ‘Report’) is prepared and distributed by Reliance Securities Limited (RSL) for information purposes only. The views herein

General Disclaimers: This Research Report (hereinafter called ‘Report’) is prepared and distributed by Reliance Securities Limited (RSL) for information purposes only. The views herein